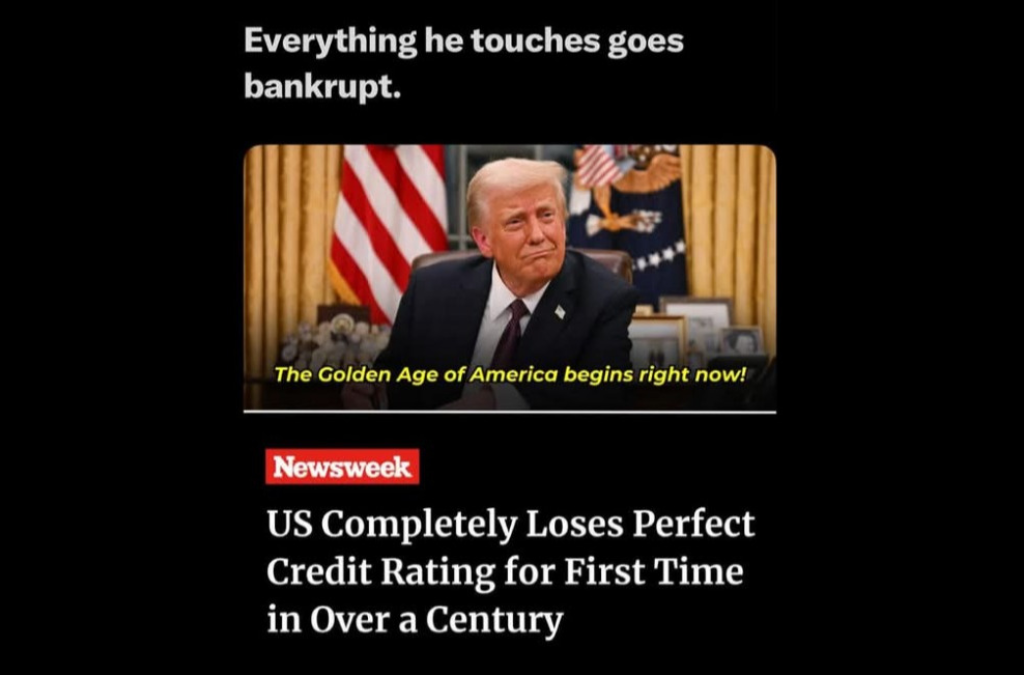

Moody’s Ratings downgraded the U.S. government’s credit rating on Friday, citing repeated failures by successive administrations to control the country’s growing debt. The agency lowered the rating from its highest grade, Aaa, to Aa1, noting that while the U.S. still benefits from key strengths—such as a dynamic economy and the global dominance of the U.S. dollar—its fiscal outlook has significantly deteriorated.

Newsweek has reached out to the U.S. Treasury Department via email on Friday afternoon for comment.

Why It Matters

The shift means the United States no longer enjoys a fully stable top-tier rating from any major agency for the first time in more than 100 years. Moody’s becomes the third and final major credit agency to reduce its assessment of the federal government’s creditworthiness. Standard & Poor’s made its first-ever downgrade in 2011, and Fitch Ratings followed in 2023.

What to Know

In its announcement, Moody’s, led by chief economist Mark Zandi, projected the federal deficit will rise to nearly 9 percent of GDP by 2035, up from 6.4 percent in 2024, driven by mounting interest payments, rising entitlement costs, and sluggish revenue growth.

Moody’s also warned that extending President Donald Trump’s 2017 tax cuts—now a key priority for the Republican-led Congress—would add $4 trillion to the federal primary deficit over the next decade. Political gridlock remains a major obstacle to fiscal reform, with Republicans opposing tax increases and Democrats resisting spending cuts, leaving little room for bipartisan solutions.

What to Know About the Three Major Credit Agencies

The three major credit rating agencies—Moody’s Investors Service, S&P Global Ratings, and Fitch Ratings—play a critical role in assessing the creditworthiness of sovereign nations, including the United States. These agencies assign ratings that influence borrowing costs, investor confidence, and global economic perceptions. A top-tier credit rating signals low risk for investors, while a downgrade can lead to increased borrowing costs and financial instability.

Historically, the U.S. maintained a perfect credit rating from all three agencies for decades, reflecting the country’s economic strength and political stability. That changed in 2011 when S&P downgraded the U.S. from AAA to AA+ following a contentious debt ceiling standoff. Fitch followed suit in 2023, citing fiscal deterioration and repeated political brinkmanship. Moody’s had been the last to maintain a stable AAA rating.

Moody’s, founded in 1909, is the oldest of the three and was created to provide investors with independent analysis of bond risk. S&P, established in 1860 and later merged into its current form, is known for its influential role in market indices and ratings. Fitch, founded in 1914, is the smallest of the three but still widely recognized in financial markets. Together, these agencies hold immense sway over global finance, and their recent assessments of the U.S. reflect growing alarm over debt levels and political instability.

What People Are Saying

Democratic strategist Chris Jackson posted on X, formerly Twitter, “BREAKING: In a stunning move, Moody’s has downgraded the U.S. credit rating from Aaa to Aa1—for the first time in history. That’s right: the only major credit agency that hadn’t downgraded us under Trump just did. Who else enjoying all this ‘economic winning’ under Trump?”

Steven Cheung, assistant to President Trump and White House Director of Communications, posted on X, “Mark Zandi, the economist for Moody’s, is an Obama advisor and Clinton donor who has been a Never Trumper since 2016. Nobody takes his “analysis” seriously. He has been proven wrong time and time again.”